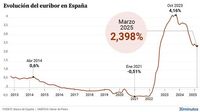

The Euribor has closed the month of March 2025 with a monthly average of 2.398%, a slight decrease of 0.009 percentage points from the February rate of 2.407%. On March 31, 2025, the Euribor adjusted downwards to 2.306%, breaking below the 2.4% threshold for the first time since September 2022. This change brings significant relief to those with variable-rate mortgages, potentially saving them up to 2,500 euros annually based on the average mortgage amount.

The impact of this adjustment is particularly notable for borrowers whose last revision was based on the March 2024 Euribor rate of 3.718%. Those homeowners will see their monthly payments decrease by between 100 and 200 euros, depending on whether their mortgage amount is 150,000 or 300,000 euros, respectively. This calculation assumes a 30-year repayment term with an interest rate of Euribor plus a differential of 0.99%.

For borrowers whose mortgages are reviewed semi-annually, the savings will be less significant, given that the Euribor was at 2.69% in October 2024. However, the overall trend indicates a positive shift in mortgage payments, even if the reductions do not completely offset the increases seen in previous years.

Despite the modest reduction this month, experts believe the Euribor is stabilizing, as noted by Simone Colombelli, director of Hipotecas at iAhorro. He stated, "This month the Euribor has shown us once again that we cannot predict its evolution because its trend can change significantly in just a week. This indicator is highly influenced by what happens politically, socially, and economically in Europe, which is why it surprises us." Colombelli further explained that the current stabilization is expected after the drastic falls experienced in prior months.

Looking ahead, the think tank Funcas predicts a Euribor rate of 2.2% for 2025, while Bankinter is more optimistic, forecasting a drop to 2.1%. Caixabank shares this sentiment, anticipating rates around 2% by the end of 2025, provided inflation remains under control and the European Central Bank (ECB) continues its monetary easing strategy.

The mortgage market is closely monitoring the ECB's next steps, particularly after the central bank has implemented six interest rate cuts since June 2024, lowering rates to 2.5%. The next decision will be revealed on April 17, 2025, when it will be determined whether the ECB will maintain the current rate or opt for another reduction.

Colombelli expressed caution regarding the upcoming ECB meeting, suggesting that it is likely the central bank will keep rates steady at 2.5% in April and may not implement further cuts until summer. He noted, "If this happens, banks will also not make significant adjustments to their offers until then. Some financial institutions are being more aggressive with interest rates for certain profiles, offering fixed rates as low as 1.80% TIN for premium customers with low debt ratios. However, generally, we do not expect dramatic changes in offers."

Should the ECB decide to cut rates next month, this would be welcomed by the mortgage market, as it could lead to further decreases in the Euribor and encourage banks to lower their mortgage rates, making it an even better time to secure a mortgage.

In March, the Euribor also reflected global economic uncertainties, particularly influenced by the recent geopolitical dynamics following the election of U.S. President Donald Trump. This uncertainty has led to fluctuations in the Euribor, which is critical for determining interest rates on various financial products, especially variable-rate mortgages in Spain.

According to the Banco de España, banks are currently accelerating the granting of credit to families and businesses as a result of the ECB's lower interest rates, which in turn affects the Euribor. The easing of mortgage and loan costs is intended to support business investment and household consumption, while also facilitating access to housing. However, there is concern that this could lead to overheating in housing prices, which have already surged in major cities and tourist destinations.

Recent data indicates that the volume of new mortgages fell to 120,000 euros in 2023 but has since risen to slightly over 160,000 euros on average. The robust demand for housing, coupled with supply limitations, has driven prices up, resulting in an annual increase of 11.3% by the end of 2024, according to experts from the Banco de España.

As the housing market continues to evolve, the dynamics of the Euribor will remain a focal point for both homeowners and potential buyers, emphasizing the importance of keeping a close eye on financial trends and central bank policies.