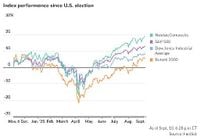

Wall Street’s mood was unmistakably upbeat on September 11, 2025, as U.S. stock markets soared to fresh record highs, powered by a potent mix of investor optimism, pivotal inflation data, and the prospect of imminent Federal Reserve rate cuts. The Dow Jones Industrial Average surged 1.3%, closing above the 46,000 mark for the first time in its history, while the S&P 500 climbed 0.9% and the Nasdaq Composite advanced 0.7%, both notching new all-time highs, according to The Wall Street Journal and The Economic Times.

It wasn’t just the giants that were rallying. The Russell 2000, a key barometer for small-cap stocks, jumped 1.8% to its highest level of the year, reflecting a broad-based enthusiasm that extended well beyond the usual suspects in technology. Even cryptocurrencies joined the party, with Bitcoin and Ethereum prices rising, while bonds rallied and yields fell across the board. The 10-year Treasury yield dropped to 4.0%, a move that caught the attention of both traders and economists, as reported by Investopedia.

The day’s optimism was anchored by the release of the August Consumer Price Index (CPI), a closely watched inflation gauge. The Bureau of Labor Statistics reported that headline inflation accelerated to 2.9% year-over-year, up from 2.7% in July, marking the highest level since January. Core inflation, which strips out volatile food and energy prices, held steady at 3.1%. While the monthly CPI increase of 0.4% was a touch hotter than the 0.3% economists had predicted, the annual figures matched expectations, giving investors confidence that inflation, while sticky, was not spiraling out of control.

“Circumstances suggest that worries over rising national claims are misplaced,” wrote Bespoke Investment Group, as quoted by The Wall Street Journal, referencing concerns over the labor market. Indeed, the jobs picture was mixed: weekly jobless claims rose by 27,000 to 263,000—the highest since October 2021—driven in part by a surge in Texas. Still, analysts cautioned that if Texas were excluded, the national claims picture looked far less alarming.

The inflation data and labor market signals have left the Federal Reserve in the spotlight. With the Federal Open Market Committee set to meet on September 17, markets are now pricing in a near-certain 25 basis point rate cut, with some traders even speculating about a larger 50 basis point move. According to Bloomberg and Investopedia, 82% of traders expect a total of 75 basis points in cuts by year’s end. “A quarter-point cut is a layup and the number still keeps a half-point cut on the table, especially when looking at the jobless data,” said Jay Woods, chief market strategist at Freedom Capital Markets.

But the path ahead is not without uncertainty. President Donald Trump’s trade policies, particularly new tariffs on imports from China and India, have begun to bite. Inflation has steadily risen this year as businesses pass on the costs of these sweeping import taxes to consumers. “With buffer inventories that had been built ahead of tariffs being depleted, businesses are now forced to replenish stock at elevated prices,” explained Katy Stoves, investment manager at Mattioli Woods. The impact is showing up in everything from coffee prices to raw materials, adding a layer of complexity to the Fed’s decision-making.

Adding to the intrigue, the composition of the Fed’s voting committee is in flux. President Trump recently attempted to fire Fed Governor Lisa Cook, citing allegations of mortgage fraud—a move without precedent. A federal judge ruled that Cook could remain in her post while her lawsuit plays out, but the administration is appealing. Meanwhile, Trump’s nominee to fill another vacancy, Stephen Miran, could be confirmed as soon as the day before the Fed’s meeting. Every vote could matter as the central bank weighs the dual mandate of fighting inflation and supporting employment.

On the corporate front, tech stocks continued to drive market sentiment. Oracle’s stock stole the show with a 36% surge on Wednesday, its best day since 1992, after reporting a backlog nearing half a trillion dollars and blowout earnings. Although shares slipped 6% on Thursday, Wall Street remains bullish. Deutsche Bank analysts called Oracle’s results “truly awesome,” while Citi dubbed the firm a “unique megacap AI winner.” The excitement is fueled by reports that OpenAI, the maker of ChatGPT, struck a $300 billion deal for Oracle’s computing power over five years, starting in 2027—though Oracle declined to comment.

Other tech names had a mixed session. Tesla jumped 6%, Apple rose over 1%, while Microsoft and Alphabet ticked higher. Nvidia, Amazon, Meta, and Broadcom saw marginal declines. Synopsys rebounded 13% after a bruising 36% drop the previous day, as analysts suggested the selloff was overdone.

Elsewhere, Warner Bros. Discovery shares rocketed 29% on reports that Paramount Skydance was preparing a takeover bid, a potential deal that could reshape the streaming and entertainment landscape. Micron Technology shares leapt 8% after Citi raised its price target, citing strong demand for memory chips and AI exposure. Opendoor Technologies, a favorite among retail investors, soared 50% after naming a new CEO and bringing its co-founders back to the board, along with a fresh $40 million cash infusion.

Commodities were more subdued. Oil prices slipped, with Brent crude steady around $67 per barrel and West Texas Intermediate down 2.3% to $62.25, following an increased global supply forecast. Gold futures dipped 0.2% to $3,673 an ounce, while the U.S. dollar index fell 0.3%.

Wall Street strategists are now scrambling to revise their forecasts. Deutsche Bank raised its year-end S&P 500 target to 7,000, citing resilient earnings and the AI boom, while Barclays also bumped up its targets, albeit with more caution over “emerging labor market risks.” Both banks agree that the promise of rate cuts and strong corporate profits could keep the bull market charging ahead, though the path may be bumpier as tariffs and inflation linger.

For investors, the message is one of cautious optimism. As the Federal Reserve prepares for its crucial meeting, all eyes are on inflation, jobs, and the shifting sands of global trade. With so many moving parts, volatility is almost guaranteed—but for now, Wall Street is betting that the worst of inflation is behind us and that lower rates will keep the rally alive.

As the dust settles on a historic day for U.S. markets, the stakes for next week’s Fed decision—and the broader economic outlook—have rarely felt higher.